International. The size of the global cooling district market is estimated to be $21.88 billion in 2018 and is expected to reach $39.94 billion by 2026, exhibiting a CAGR of 7.77% during the forecast period, according to the Fortune Business Insights report.

International. The size of the global cooling district market is estimated to be $21.88 billion in 2018 and is expected to reach $39.94 billion by 2026, exhibiting a CAGR of 7.77% during the forecast period, according to the Fortune Business Insights report.

Cooling districts are a proven and sophisticated solution that has been implemented for many years in a growing number of cities around the world. In several countries in the Middle East and North America, such as the United Arab Emirates, Saudi Arabia, Qatar, the United States and in some parts of Asia Pacific, such as China, Japan, Singapore, etc., a considerable amount of refrigeration is supplied through district refrigeration networks. The cooling district emerged as an essential product to provide a local, accessible, low-carbon cooling supply.

It represents a significant opportunity for growing cities to move towards climate-resilient, resource-constrained, low-carbon pathways. Improving energy efficiency and renewables in the global energy mix is the biggest contribution to keeping the global temperature rise below 2°C. District cooling provides chilled water through an integrated system for cooling purposes in educational institutes, hospitals, commercial buildings, industries and many more.

A centralized system produces cooled water, and cooling energy is supplied in the form of chilled water through a system of underground pipes to the consumer's location. District cooling can be more than twice as efficient as the traditional decentralized air conditioning system and can reduce electricity use during the peak demand period through reduced energy consumption. Consequently, the demand for the district's cooling system is increasing rapidly, and there is huge market potential in the coming years due to drastic changes in the earth's temperature.

The district's cooling system can increase resilience and access to energy through its ability to improve electricity demand management and adapt to frequent fuel price shocks. Incorporating domestic utilities into a business model, such as through full or partial ownership, is key to reaping the benefits of district cooling. In Dubai, 70% of total electricity consumption goes to air conditioning. The government is committed to meeting 40% of its cooling needs through district cooling by 2030, using 50% less electricity than a standard air conditioner.

GCC countries are dominating the size of the district cooling market in the Middle East and Africa region. Huge growth in construction, infrastructure and atmospheric temperature is playing an important role in increasing demand for district cooling systems. The substantial potential in the UAE and Saudi Arabia due to rapid urbanization coupled with ongoing construction activities, with the government's gaze on the adoption of energy-efficient technology, is driving market demand in GCC.

Qatar is experiencing similar growth in construction, followed by economic diversification for the 2022 FIFA World Cup, which is driving the growth of district cooling. A large portion of the funding to build world-class facilities for the 2022 FIFA World Cup is also projecting positive growth for this market. North America has an important market for urban refrigeration due to technological advancement and the growing need for air conditioning.

In order to mitigate GHG emissions and improve overall system performance, the United States has adopted the district cooling system to a greater extent. Drastic changes in weather conditions and rising earth temperature have rapidly increased the demand for space cooling, which is expected to increase the growth of the market.

Market indicators

The district's cooling system is highly efficient and offers sustainable cooling that helps reduce GHG emissions. A single-district cooling system can act as efficiently as hundreds of CAs.

Government entities and private companies are investing heavily in energy-efficient technology to meet the growing demand for air conditioning with reduced energy consumption. The growth of the district cooling market is driven by increasing urbanization and commercialization.

Segmentation

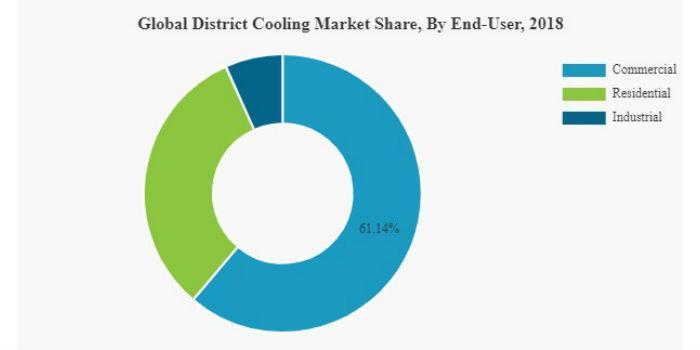

The high demand for air conditioning by commercial buildings, educational institutes, airports, IT parks, business parks, etc., is expected to take advantage of the demand for the district's cooling system. Massive investment in energy-efficient technology, coupled with a growing push for sustainable energy development, is anticipated to increase the size of the district's cooling market. The residential sectors offer a lucrative market in GCC due to the continuous deployment of large-scale projects to meet the growing demand for air conditioning. The industrial cooling market is expected to grow at a steady pace.

North America is the second largest market for urban cooling after the Middle East and Africa. Almost all airports and institutional buildings in the United States are connected through the district's refrigeration network to meet the high demand for air conditioning. China and Japan have a majority share in district cooling due to growing concerns about GHG emissions and growing demand for air conditioning. The atmospheric environment is likely to inhibit the growth of district cooling in Europe, but still some countries plan to install a district cooling project in their country.

The district cooling market is witnessing substantial growth in the MEA countries due to increasing private investment in the development of energy-efficient cooling, along with the government's initiative for sustainable energy development. The commercial and residential sector shares the substantial district cooling market due to rising energy prices along with urban population growth.

The UAE and Saudi Arabia are the largest countries in the GCC accounting for more than 75% of the total installed district cooling capacity in MEA. Qatar is investing massively in an infrastructure development project to provide a world-class facility for the scheduled 2022 FIFA World Cup. Other countries are also making a significant contribution to the district cooling market which includes Bahrain, Kuwait and Oman.

Source: Fortune Business Insights.